EU CSRD Consulting

Strategic advisory and sustainability reporting support services for companies impacted by the EU Corporate Sustainability Reporting Directive (CSRD)

We help companies to meet the EU’s new sustainability reporting legislation.

What is the European Union’s Corporate Sustainability Reporting Directive (EU CSRD)?

The Corporate Sustainability Reporting Directive was passed in November 2022 and widely affects companies headquartered or operating in the European Union (EU). As part of the 2020 European Green Deal and the EU’s larger initiative to elevate sustainability reporting to the same level and legitimacy of financial reporting, the EU CSRD strengthens the existing Non-Financial Reporting Directive (NFRD) by expanding which sustainability topics are mandatory to report and by increasing the number of affected companies from around 11,600 to over 50,000.

Affected companies will meet the CSRD through a series of preparatory steps. First, companies are required to carry out a Double Materiality Assessment to understand which sustainability topics are material from both an impact perspective and a financial perspective as applied to both the business group and value chains. Through the strict double materiality assessment requirement, the EU CSRD brings greater transparency to the social and environmental impacts associated with reporting companies, as well as their related risks.

The EU CSRD introduces the European Sustainability Reporting Standards (ESRS), which companies will use to prepare and report on ESG topics annually. The comprehensive set of 12 standards cover general requirements and disclosures applicable to all reporting entities (ESRS1 & 2) along with ESRS E1-E5 for reporting material environmental disclosures, ESRS S1 – S4 for reporting social disclosures and one standard covering corporate governance - ESRS G1. ESRS standards have been developed with interoperability across common global reporting frameworks, such as GRI and SASB. The intended result is that the sustainability disclosures offer comparable data so that investors, civil society, and other stakeholders can make better, more informed decisions.

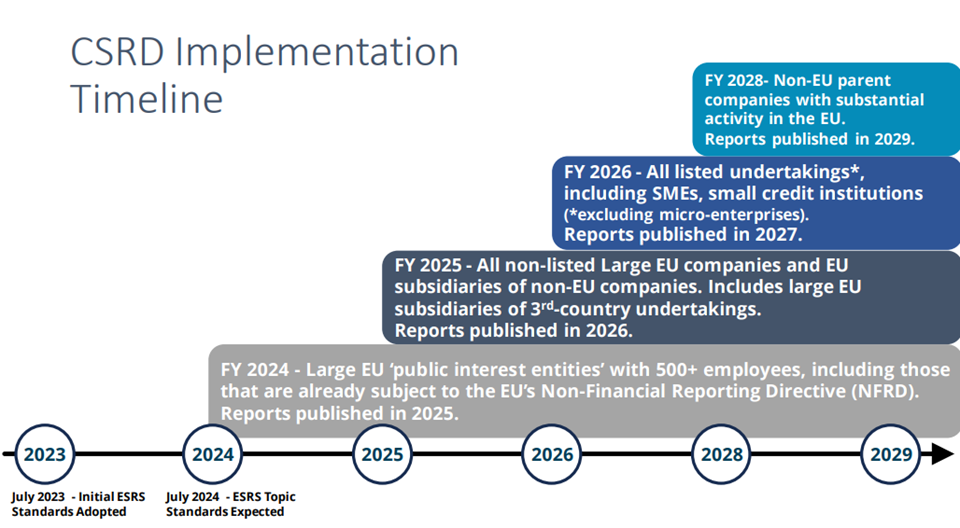

Which companies will be required to report under EU CSRD and when does reporting begin?

EU CSRD will affect an estimated 50,000 companies, including companies headquartered outside of the EU borders but with subsidiaries operating within the EU market or substantial activity within the EU. Factors determining which companies must report under CSRD include financial thresholds, such as annual net revenue, total assets held within the EU, total number of employees and for companies “listed” and admitted to trading on a regulated EU market, the amount of debt and equity securities.

Companies with specific questions about how the law will be applicable to their operations are encouraged to contact SCS Consulting today.

Steps to Achieving EU CSRD Readiness and Compliance

Achieving EU CSRD compliance will look different for every company based on each company’s unique ESG and materiality profile. SCS Consulting provides numerous steps that can be engaged during any phase of your CSRD reporting process.

- Applicability Determination: The CSRD includes implementation dates that vary by the type and size of the company. We help you to assess your business group’s legal structure against the CSRD legal requirements to understand the timeline for mandatory reporting across your business entities.

- Double Materiality Assessment: All companies reporting under CSRD will be required to carry out a comprehensive double materiality assessment. We work with your company to carry out the assessment in preparation for reporting.

- Gap Assessment: We carry out gap assessments against the double materiality results, the ESRS modules, and the relevant voluntary standards and frameworks that comprise your company’s existing reporting efforts. These include: GRI, SASB, TCFD, TNFD, GRI, ISSB, and the UN Sustainable Development Goals.

- Strategy Development: The Double Materiality Assessment results will set the scope for CSRD reporting. We work with your company to develop the strategy for integrated reporting and filling in reporting gaps, to include incorporating gap assessment results around existing reporting efforts.

- EU CSRD Report Development: We work with companies to compile and analyze disclosure data and to create the reporting content in line with the ESRS standards and any other voluntary standard or framework utilized in annual reporting. SCS Consulting supports the disclosure of information in XHTML format to ensure the information is available and accessible in accordance with the European Single Electronic Format (ESEF).

- External Assurance: SCS Consulting offers assurance readiness and consulting. If your company needs certified, third-party assurance, please visit SCS Global Services. SCS Consulting can ensure your company is prepared for mandatory, limited assurance under CSRD.

- Environmental Claims Language Review: We review report content to ensure that claims language adheres to legal requirements around anti-greenwashing, climate and sustainability claims across multiple markets (EU, USA, Canada, UK, others)

- Leverage Results to Improve: We work to leverage each reporting cycle to identify areas for improvement and to inform further development of your corporate sustainability strategy. Our goal is that your sustainability program and reporting efforts are strengthened over time.